As an expert in financial planning and tax strategy, I know firsthand the relief and confidence that comes with being fully prepared for tax season. The thought of upcoming tax deadlines can often feel daunting, but with a proactive approach, you can transform it into an organized, stress-free process. If you’re wondering how to prepare for March 2026 tax season deadlines, you’re in the right place. This guide will walk you through essential steps, helping you navigate the complexities of tax filing for the 2025 tax year and beyond, ensuring you’re ready well before those crucial dates arrive.

Preparing early isn’t just about avoiding last-minute panic; it’s about optimizing your financial situation, maximizing potential tax deductions and credits, and ensuring full compliance with IRS regulations. My experience has taught me that meticulous tax planning throughout the year is the key to a smooth filing experience. Let’s dive into how you can expertly manage your 2026 tax season responsibilities.

Understanding Key Tax Deadlines for 2026

Navigating the calendar of tax season deadlines is the first critical step in effective preparation. Missing a deadline can lead to penalties, which no one wants. For the 2025 tax year, filed in 2026, there are several important dates to keep in mind, depending on your filing status and business structure.

Key Filing Dates for Individuals and Businesses

For most individual taxpayers and C-Corporations, the primary deadline to file federal income tax returns and pay any taxes owed is typically April 15, 2026. However, March 2026 tax season deadlines are especially important for certain business structures.

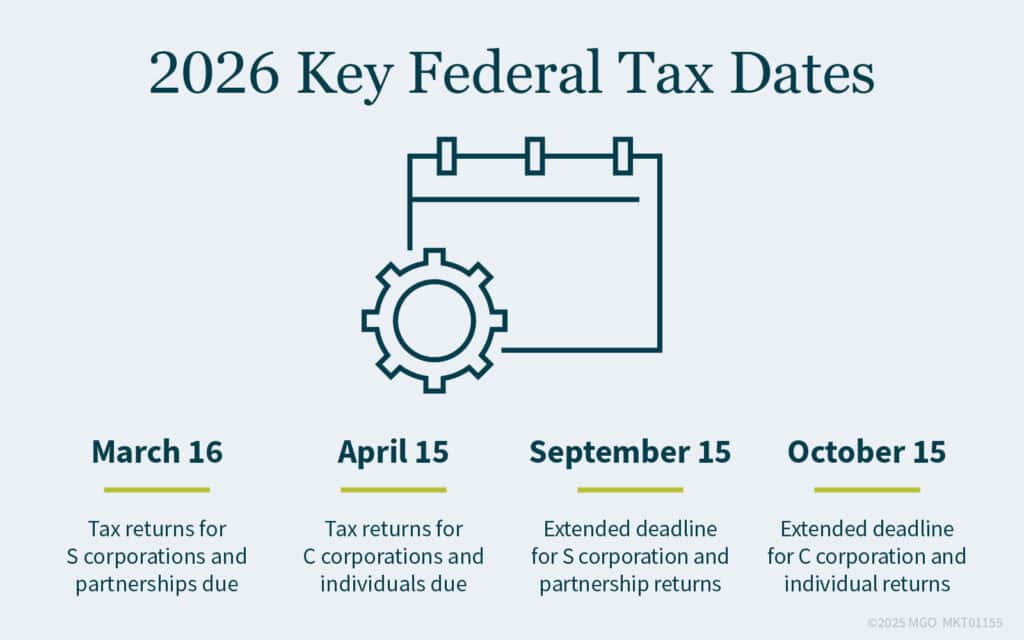

- March 15, 2026: This date is significant for S-Corporations (Form 1120-S) and Partnerships (Form 1065). If you own or operate one of these entities, your business tax return is due by this date. Proactive preparation ensures these complex returns are accurate.

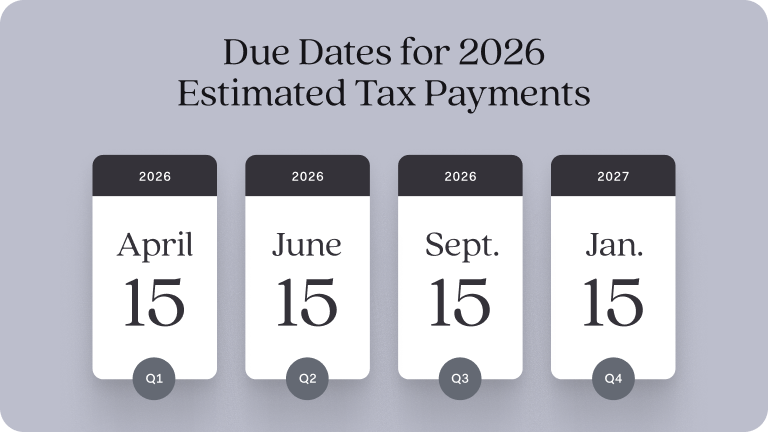

- April 15, 2026: This is the big one for most. Individuals filing Form 1040, and C-Corporations filing Form 1120, must submit their returns and pay any taxes due by this date. It also marks the deadline for making the first quarterly estimated tax payment for the 2026 tax year.

- June 15, 2026: The second quarterly estimated tax payment for the 2026 tax year is typically due.

- September 15, 2026: The third quarterly estimated tax payment for the 2026 tax year is due. This date also applies to extended S-Corporation and Partnership returns.

- October 15, 2026: If you filed for an extension for your individual income tax return or C-Corporation return, this is your final deadline. Remember, an extension to file is not an extension to pay.

- January 15, 2027: The fourth and final quarterly estimated tax payment for the 2026 tax year is due.

Understanding these dates is fundamental. Mark them clearly on your calendar. I always advise clients to aim for filing well before the actual deadline to avoid any last-minute stress or technical glitches.

The Foundation of Early Tax Preparation

The secret to a stress-free tax season lies in consistent, year-round organization. My most successful clients are those who don’t just scramble in January but maintain robust record-keeping practices throughout the year. This approach makes gathering documents for the 2025 tax year filing in 2026 a breeze.

Gathering Essential Documents

Before you can even think about filling out forms, you need your paperwork. Think of these as the building blocks of your tax return. Keep a dedicated folder, physical or digital, for all tax-related documents as they arrive.

- Income Statements: This includes your W-2s from employers, 1099-NEC for freelance income, 1099-MISC for miscellaneous income, 1099-INT for interest income, 1099-DIV for dividends, and K-1s for partnership or S-Corp income. Make sure all these are accounted for.

- Investment and Retirement Account Statements: Brokerage statements (Form 1099-B) detailing stock sales and capital gains/losses, and statements for IRA or 401(k) contributions are crucial. These impact your taxable income.

- Mortgage Interest Statements: Form 1098 shows the mortgage interest you paid, which is often a significant itemized deduction.

- Student Loan Interest: Form 1098-E details interest paid on student loans, another potential deduction.

- Health Insurance Information: Form 1095-A, 1095-B, or 1095-C, depending on your health coverage, is needed for healthcare-related credits and compliance.

- Property Tax Records: If you own property, gather statements showing property taxes paid.

- Childcare Expenses: Records of payments made to childcare providers, along with their Tax ID numbers, are necessary for the Child and Dependent Care Credit.

Organizing Financial Records Effectively

Beyond the official forms, you’ll need a clear system for receipts and other financial transactions. This is particularly vital for small business owners and self-employed individuals claiming business expenses.

I recommend categorizing expenses as they occur. Whether you use a spreadsheet, accounting software like QuickBooks, or a simple folder system, consistency is key. Documenting charitable donations, medical expenses, and business mileage throughout the year saves immense time and stress come tax time. Digital scanning of receipts is a game-changer for many of my clients, allowing for easy search and backup.

Maximizing Deductions and Credits

This is where smart tax planning truly shines. Understanding and claiming every eligible tax deduction and credit can significantly reduce your tax liability or increase your tax refund. It requires a bit of knowledge and careful record-keeping.

Common Individual Deductions to Consider

Many individuals overlook valuable deductions. These reduce your taxable income, meaning you pay taxes on a smaller portion of your earnings.

- Standard vs. Itemized Deductions: You’ll choose whichever provides a greater benefit. Itemizing requires careful tracking of expenses like state and local taxes (SALT cap applies), mortgage interest, charitable contributions, and medical expenses (if exceeding a certain percentage of AGI).

- Student Loan Interest Deduction: Up to $2,500 of student loan interest paid can be deducted.

- IRA Contributions: Contributions to a traditional IRA can be tax-deductible, reducing your current year’s taxable income.

- Health Savings Account (HSA) Contributions: If eligible, contributions to an HSA are tax-deductible.

Business Deductions for Self-Employed and Small Businesses

Self-employed individuals and small business owners have a broader range of potential deductions. This is a critical area where proper record-keeping directly impacts your bottom line.

- Home Office Deduction: If you use a part of your home exclusively and regularly for business, you may qualify. Ensure you meet the IRS criteria.

- Business Expenses: This includes supplies, advertising, professional development, software subscriptions, and travel expenses directly related to your business. Keep meticulous records of all such outlays.

- Health Insurance Premiums: If you’re self-employed, you might be able to deduct the premiums you paid for health insurance for yourself, your spouse, and your dependents.

- Retirement Plan Contributions: Contributions to a SEP IRA, Solo 401(k), or SIMPLE IRA can be powerful tax-savers for business owners.

Exploring Valuable Tax Credits

Unlike deductions, which reduce taxable income, credits directly reduce the amount of tax liability you owe, dollar for dollar. Some credits are even refundable, meaning you could get a refund even if you owe no tax.

- Child Tax Credit: A significant credit for eligible families with qualifying children.

- Earned Income Tax Credit (EITC): A refundable credit for low-to moderate-income working individuals and families.

- Education Credits: The American Opportunity Tax Credit and Lifetime Learning Credit can help offset higher education expenses.

- Energy Credits: Credits for making energy-efficient home improvements or purchasing electric vehicles.

- Child and Dependent Care Credit: For expenses paid for the care of a qualifying individual to allow you to work or look for work.

It’s vital to research which credits apply to your unique situation. A simple chart can help you visualize the difference and potential impact:

| Feature | Tax Deduction | Tax Credit |

|---|---|---|

| Impact on Taxes | Reduces Taxable Income | Directly Reduces Tax Owed |

| Value | Based on your Marginal Tax Rate (e.g., $100 deduction saves $24 for someone in 24% bracket) | Dollar-for-Dollar Reduction (e.g., $100 credit saves $100) |

| Refundable Potential | Generally No | Some credits (e.g., EITC, Child Tax Credit) can be refundable |

| Eligibility | Typically broader criteria, but requires sufficient expenses to exceed standard deduction if itemizing | Specific criteria often tied to income, family status, or specific activities |

Strategic Tax Planning for 2025 (Filing in 2026)

Good tax preparation isn’t just about looking backward; it’s about making strategic decisions throughout the year that positively impact your future tax liability. This proactive approach is a cornerstone of effective personal finance management.

Reviewing Estimated Tax Payments

If you’re self-employed or have significant income not subject to withholding, you likely make quarterly estimated tax payments. Reviewing these payments periodically throughout 2025 is crucial to avoid underpayment penalties. Adjust your estimates if your income or deductions change significantly. This keeps you in good standing with the IRS.

Optimizing Retirement Contributions

Contributing to retirement accounts like a 401(k) or traditional IRA is one of the most effective ways to reduce your taxable income. For the 2025 tax year, be mindful of contribution limits and try to max them out if possible. Even small contributions can add up to substantial tax savings over time.

Leveraging Health Savings Accounts (HSAs)

For those with high-deductible health plans, an HSA is a triple tax-advantageous account. Contributions are tax-deductible, earnings grow tax-free, and qualified medical withdrawals are tax-free. It’s a powerful tool for both healthcare savings and tax planning.

Managing Capital Gains and Losses

If you invest in taxable brokerage accounts, strategically managing capital gains and losses can impact your tax bill. Tax-loss harvesting, where you sell investments at a loss to offset gains, can be a valuable strategy. Discuss this with a financial advisor to understand its implications for your specific portfolio.

Leveraging Technology and Professional Help

In today’s digital age, numerous tools and resources can simplify tax preparation. Knowing when to use software and when to consult a human expert is a key part of smart tax strategy.

Choosing the Right Tax Software

For many individuals with straightforward returns, tax software like TurboTax, H&R Block, or FreeTaxUSA can be an excellent, cost-effective solution. These platforms guide you through the process, automatically calculating deductions and credits based on your input. They are designed for user-friendliness and can e-file your return directly with the IRS.

When selecting software, consider:

- Your Complexity: Do you have investments, a small business, or just a W-2?

- Cost: Free versions exist for simple returns; more complex situations require paid tiers.

- Support: Some offer live help from tax professionals.

When to Consult a Tax Professional

While software is great, there are times when the expertise of a CPA (Certified Public Accountant) or Enrolled Agent (EA) is invaluable. I always advise clients to seek professional help if they:

- Have significant life changes (marriage, divorce, new child, home purchase).

- Start a new business or have complex business structures.

- Have international income or assets.

- Are dealing with an IRS audit or tax notices.

- Want advanced tax planning strategies or estate planning advice.

A good tax professional can identify deductions you might miss, ensure compliance, and offer strategic advice tailored to your financial goals. Their fees are often well worth the peace of mind and potential tax savings.

Avoiding Penalties and Common Mistakes

No one wants to pay more than they owe, especially in penalties. Understanding common pitfalls and how to avoid them is a crucial aspect of how to prepare for March 2026 tax season deadlines effectively.

Understanding Underpayment Penalties

If you don’t pay enough tax throughout the year through withholding or estimated tax payments, you could face an underpayment penalty. The IRS generally requires you to pay at least 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% if your AGI was over $150,000) to avoid this. Regularly reviewing your income and adjusting withholdings or estimated payments is key.

Preventing Late Filing and Late Payment Penalties

As mentioned earlier, deadlines are strict. A late filing penalty can be steep, typically 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25%. A late payment penalty is usually 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25%. Filing an extension prevents the late filing penalty but not the late payment penalty. Always pay what you owe by the original deadline.

Ensuring Accuracy and Being Prepared for Audits

The most common mistake is simply making errors. Double-check all entries, especially Social Security numbers, bank account details for refunds, and income figures. Keep all supporting documentation organized for at least three years, as the IRS has up to three years to audit your return. Being able to quickly provide requested documents can make an audit a less stressful experience.

Conclusion

Preparing for the March 2026 tax season deadlines and beyond doesn’t have to be a stressful annual event. By adopting a proactive, organized, and informed approach, you can transform it into an opportunity for financial clarity and optimization. Start early, gather your documents systematically, explore every eligible deduction and credit, and leverage both technology and professional expertise when needed. My personal experience has shown that those who plan ahead not only avoid penalties but often uncover significant savings. Take control of your taxes now, and enjoy the peace of mind that comes with being thoroughly prepared for the 2025 tax year filing season. Remember, the journey to a smooth tax season begins long before the deadlines hit.

Frequently Asked Questions

What are the most critical tax deadlines for March 2026?

For March 2026, the most critical deadline is March 15th, 2026, which is typically when S-Corporations (Form 1120-S) and Partnerships (Form 1065) must file their federal income tax returns. While the general individual deadline is April 15th, business owners need to pay close attention to the March date.

What documents should I start gathering now for the 2025 tax year (filed in 2026)?

Start collecting all income statements like W-2s, 1099s (NEC, MISC, INT, DIV), and K-1s. Also, gather investment statements, mortgage interest statements (Form 1098), student loan interest statements (Form 1098-E), health insurance forms (1095-A, B, or C), property tax records, and receipts for charitable donations or business expenses. Consistent organization throughout the year is key.

How can self-employed individuals best prepare for the March 2026 tax season deadlines?

Self-employed individuals should meticulously track all income and expenses, make timely quarterly estimated tax payments to avoid underpayment penalties, and explore all eligible business deductions such as home office expenses, health insurance premiums, and contributions to self-employed retirement plans like a SEP IRA or Solo 401(k). Consider consulting a CPA for tailored advice.

What’s the difference between a tax deduction and a tax credit, and why is it important for tax preparation?

A tax deduction reduces your taxable income, meaning you pay tax on a smaller portion of your earnings (e.g., a $1,000 deduction for someone in a 24% tax bracket saves $240). A tax credit, on the other hand, directly reduces the amount of tax you owe, dollar-for-dollar (e.g., a $1,000 credit saves $1,000). Understanding this difference is crucial for maximizing your savings and accurately calculating your tax liability or refund.